》View SMM Lead Product Quotations, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

》Click to Access the SMM Database

SMM, February 15:

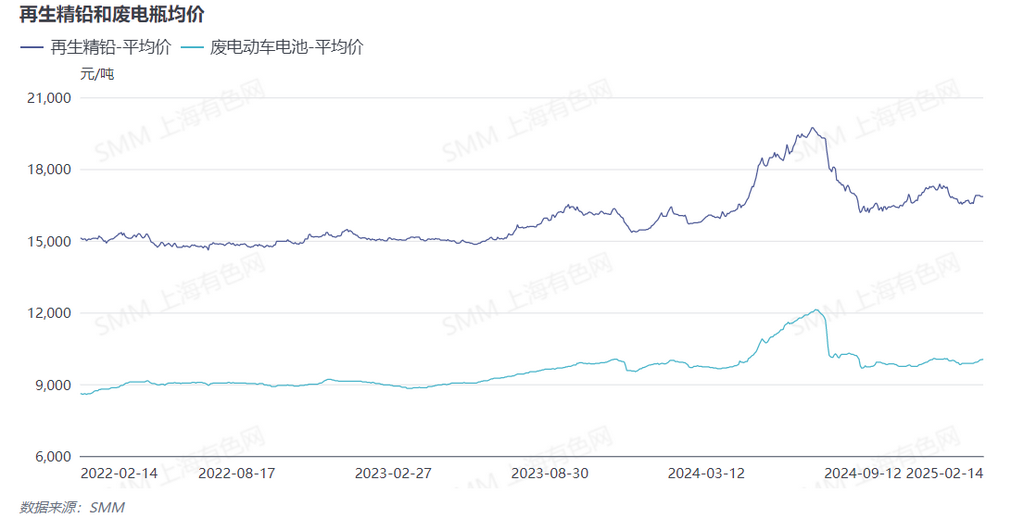

During the Chinese New Year holiday, downstream battery producers generally suspended operations, leading to extremely low demand for lead ingots. This resulted in secondary lead smelters being unable to sell their finished products in a timely manner, causing a significant accumulation of finished product inventories. After the holiday, lead prices fluctuated at high levels, and suppliers followed the market trend, quoting premiums of 0-50 yuan/mt against the SMM 1# lead average price. However, as downstream battery producers resumed operations later than usual, their enthusiasm for purchasing lead ingots remained low. Secondary lead smelters generally reported difficulties in closing deals, leading to a gradual loosening of quotations.

Last week, some secondary lead smelters quoted ex-factory prices for high-bismuth lead at discounts of around 50 yuan/mt against the SMM 1# lead average price; this week, the discounts could widen to 150-75 yuan/mt. Even so, downstream battery producers' purchase willingness remained moderate.

It is understood that a large lead-acid battery producer restocked lead ingots at low prices before the holiday, purchasing a significant amount. During the holiday, the company was mostly shut down, and with low operating rates after the holiday, its lead ingot inventory was only slightly consumed. As a result, it is expected to have almost no external purchase demand for lead ingots in mid-to-late February, significantly affecting the destocking of lead ingots. High social and in-plant inventories of lead ingots are likely to limit lead price movements.

As next Monday marks the delivery date for the SHFE lead 2502 contract, social inventories of lead ingots are expected to increase further. In the short term, bearish factors outweigh bullish factors for lead prices. Currently, the main support for lead prices comes from scrap lead-acid batteries. Due to the off-season for scrapping lead-acid batteries and the concentrated post-holiday resumption of secondary lead smelters, the undersupply situation is expected to drive significant price increases.

In summary, with the expected increase in social inventories for delivery next week and the lackluster sentiment in downstream consumption, the most-traded SHFE lead contract may have a chance of falling below 17,000 yuan/mt. However, due to the cost support from secondary lead raw materials, the decline in lead prices may be limited.